Capital Follows Authority

The AI Capital Cycle - and How Sponsors Now Control Enterprise AI

Most investors are still analyzing artificial intelligence as if it were a product cycle.

They are asking which model is better, which chip is faster, which company will beat quarterly expectations.

That is not how enterprise spend is routed.

Enterprise spend is routed through authority.

And if you are allocating capital across long-duration assets… across currencies, across liquidity regimes, across cycles… authority is the only layer that matters.

So I started somewhere different.

I wanted to know whether enterprise AI is being adopted as a growth catalyst inside business units, or whether it is being embedded inside restructuring mandates and operating-model enforcement.

If it is the latter, then the institutions that sit at the enforcement layer of the capital stack should be building capacity, and the layers dependent on labor expansion should not be in synchronized breakout mode.

That is testable.

So I mapped the entire routing system.

Private equity platforms: Blackstone, Apollo, KKR, Carlyle, Bain Capital, TPG, Warburg Pincus, Silver Lake, Vista, Thoma Bravo.

Strategy and transformation firms: McKinsey, Bain, BCG, Accenture, Capgemini.

Big Four advisory: Deloitte, PwC, KPMG, EY-Parthenon.

Restructuring and performance improvement specialists: Alvarez & Marsal, AlixPartners, FTI.

Capital advisory boutiques: Evercore, Lazard, PJT, Moelis, Houlihan Lokey.

Enterprise application vendors across ERP, HCM, CRM, procurement and workflow.

AI-native data platforms and infrastructure.

Global delivery and labor-arbitrage firms.

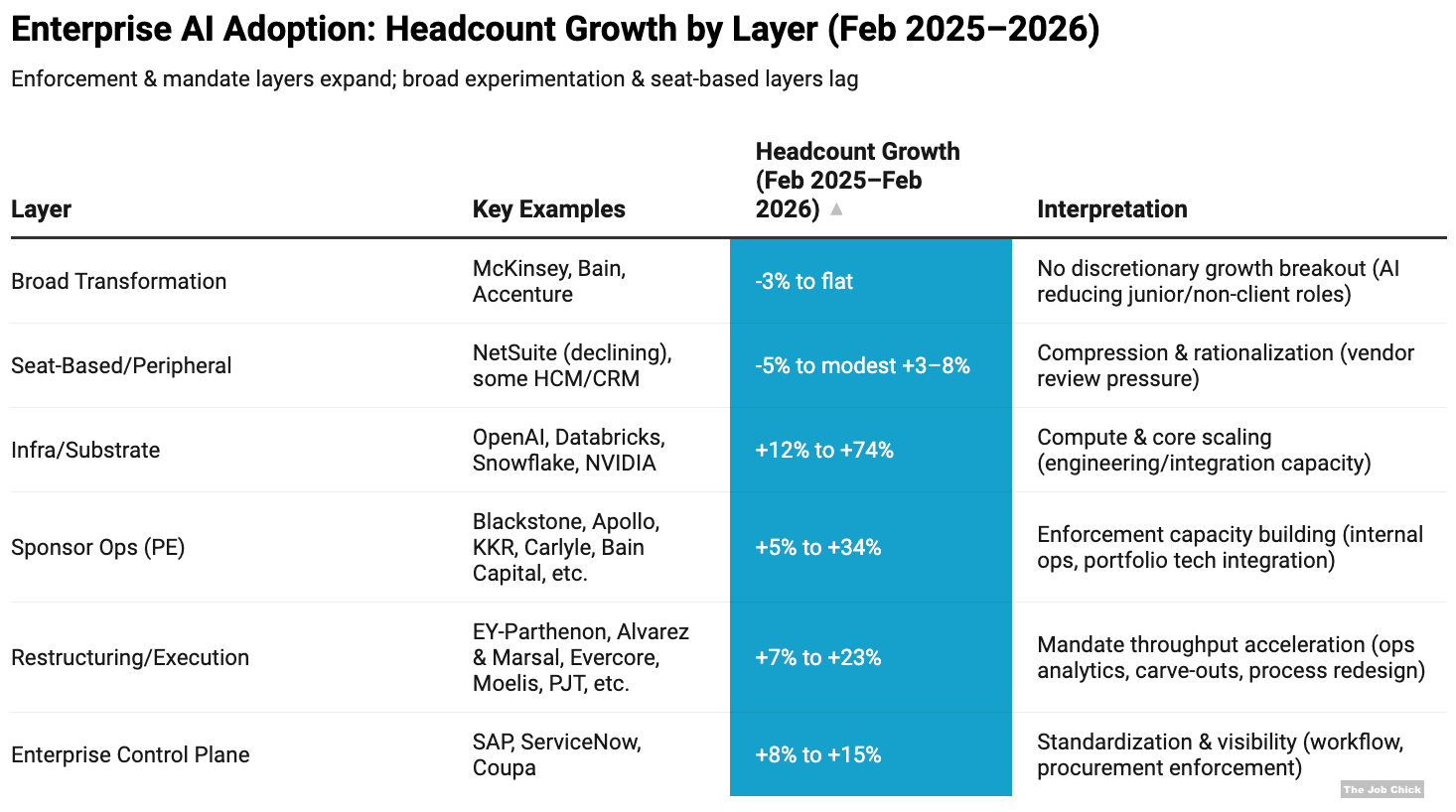

If AI were primarily a bottom-up innovation cycle, you would expect to see broad hiring acceleration across implementation firms, offshore delivery, and seat-based SaaS vendors. If instead AI is being embedded inside cost programs written by sponsors and restructuring firms, you would expect to see expansion concentrated in those layers.

The staffing data is not ambiguous.

Between February 2025 and February 2026 (YTD):

Blackstone increased internal headcount by +33.81%.

Apollo expanded +15.43%.

KKR +12.53%.

Carlyle +10.28%.

Bain Capital +8.35%.

Warburg Pincus +7.09%.

Thoma Bravo +7.18%.

Silver Lake +5.49%.

TPG +6.65%.

From a workforce composition standpoint, that magnitude of growth inside private equity is not cyclical enthusiasm. It reflects an institutional decision to intensify internal control. These hires are not junior deal teams chasing IPO windows… they are portfolio operations leads, technology integration officers, centralized procurement analysts, margin modeling specialists, data governance heads and cross-portfolio reporting teams.

When sponsors expand internal operating teams double digits during a constrained exit environment, they are not preparing for optionality… they are preparing for enforcement.

And for a multi-billion allocator, that matters.

Enforcement capacity reduces dispersion inside portfolios while increasing dispersion across vendors.

More sponsor oversight means:

• Vendor stacks are reviewed centrally.

• Tech budgets are scrutinized centrally.

• Automation targets are standardized.

• Labor cost benchmarks are enforced.

That creates a capital-routing bottleneck…

Now move one layer down.

EY-Parthenon expanded +23.14%.

Alvarez & Marsal +21.17%.

Evercore +14.64%.

Moelis +10.83%.

PJT +10.70%.

Lazard +8.70%.

Houlihan Lokey +7.43%.

Deloitte +11.54%.

This is not broad consulting optimism at all… its just good ol’ fashioned throughput. These firms scale when cost programs move from slide decks to execution schedules, and from a workforce perspective, this represents expansion in:

Operational analytics teams.

Restructuring associates.

Vendor rationalization specialists.

Carve-out implementation leads.

Process redesign engineers.

When this layer thickens simultaneously with sponsor operating teams, it means decision velocity increases. For allocators thinking in duration terms, that implies AI deployment is not happening through experimentation budgets. It is happening through mandate pipelines.

Now contrast that with McKinsey at −1.95%, Bain flat at −0.14%, and Accenture at −3.12%.

If AI were a discretionary growth theme, the broad transformation houses would be in breakout hiring mode. They are not.

The growth is concentrated in enforcement-adjacent execution.

Now look at enterprise software.

ERP:

SAP +13.74%.

Oracle +1.71%.

NetSuite −5.54%.

SAP reinforcing core control systems makes sense in an environment where financial reporting and cost visibility matter more. Oracle holding steady is not an expansion story. NetSuite contracting tells you mid-market tightening is real.

HCM:

Workday +3.63%.

ADP +2.57%.

UKG +9.85%.

Dayforce +10.88%.

If companies were preparing for a hiring boom, these numbers would look very different. Instead, this looks like instrumentation… labor tracking, scheduling automation, payroll consolidation.

CRM:

Salesforce +7.75%.

Workflow:

ServiceNow +15.22%.

When processes are standardized and enforced, workflow becomes central.

Procurement:

Coupa +8.82%.

Spend management scaling fits cost discipline cycles.

Now underneath that layer:

OpenAI +74.37%.

Databricks +29.59%.

Snowflake +16.99%.

NVIDIA +12.24%.

The substrate is scaling.

Now look at global delivery.

Cognizant −2.26%.

Infosys +14.55%, but not part of a synchronized offshore explosion.

If this were an outsourcing-led transformation cycle like 2014–2019, offshore hiring would be accelerating aggressively. It isn’t.

Compute is scaling, enforcement capacity is scaling, labor intensity is not scaling proportionally… and that alignment is not random.

This is critical.

Revenue streams tied to measurable cost reduction embedded in sponsor mandates behave differently in tightening liquidity environments than revenue streams tied to hiring growth and discretionary expansion.

When AI is embedded in restructuring decks, it becomes:

Non-discretionary.

Capital-aligned.

Portfolio-standardized.

All of those increases durability for substrate layers.

It also increases concentration risk for peripheral SaaS, and compression risk for seat-based vendors dependent on headcount expansion.

Now, for a moment, consider vendor rationalization across sponsor portfolios.

If a sponsor controls 20 portfolio companies and eliminates two overlapping $1M SaaS vendors per company, that is $40M displaced within one platform.

Across ten major sponsors, that is $400M displaced, and that displacement does not hit the ERP control plane first. It hits peripheral tools, which increases dispersion, and from a capital allocation standpoint, dispersion creates asymmetry.

Infrastructure embedded in cost mandates retains support.

Peripheral expansion tools face consolidation pressure.

Now return to my thesis.

Whoever controls the consultant controls enterprise AI spend.

Consultants write the restructuring deck.

Sponsors increasingly control the consultants through expanded internal operating teams.

The workforce data shows sponsor capacity thickening materially.

That means consultants are operating within tighter capital frameworks. If OpenAI partnerships are embedded in that consultant layer, AI routing becomes structural. We have arrived to this point now.

This makes everything mandate driven.

Pretty thematic overall, no?

What we are seeing is a regime shift in how enterprise capital is deployed.

Authority has moved upstream, and the enforcement layer has thickened. We are also seeing that the expansion-dependent layers have not accelerated proportionally.

This is a total reconfiguration of the enterprise operating system, and capital always follows the layer that can enforce change.

Now… let’s push the capital implications further from a workforce POV.

If authority is consolidating at the sponsor and restructuring layer, and if AI deployment is being routed through mandate rather than experimentation, then duration risk across enterprise technology bifurcates.

That bifurcation is not visible in quarterly earnings, but it is visible in how revenue is justified internally. Let’s not forget that revenue justified as cost reduction behaves quite differently from revenue justified as growth enablement. In tighter liquidity, like, persistent high rates, currency volatility, boards will accelerate cost programs - favoring embedded infra (lower cut risk) over edge SaaS (higher discretionary review).

When a restructuring team embeds automation inside a portfolio-wide cost program, the internal approval process shifts. The conversation becomes: “What measurable labor savings does this generate?” rather than “Does this accelerate revenue?” That changes budget classification. Cost programs are rarely optional. Growth programs often are.

Over a five-year horizon, even modest labor compression compounds.

Assume 5 million enterprise employees across large sponsor-influenced enterprises. If AI-enabled automation reduces aggregate headcount by 1% per year over five years, that is roughly 50,000 seats per year, compounding. After five years, roughly 250,000 seats have been removed relative to baseline. At $220 per seat annually, that is $55 million in normalized HCM revenue displacement relative to trend. At 2% annual compression, the compounding effect doubles.

The point is not that HCM collapses.. it’s that marginal seat growth embedded in long-duration valuation models becomes structurally lower.

Now layer in vendor rationalization.

If each major sponsor portfolio eliminates two peripheral SaaS tools per asset over a three-year window, and average ACV is $1 million per tool, the math is straightforward. For a 20-company portfolio, that is $40 million displaced. For ten large sponsors executing similar rationalization programs, $400 million in recurring SaaS revenue is redistributed or eliminated. This does not mean all revenue disappears. Some consolidates into control-plane vendors. Some shifts into standardized workflow. But the edge contracts.

Duration-sensitive capital notices edge contraction before it shows up in broad sector multiples.

Now consider margin durability.

Infrastructure providers and AI-native platforms embedded in cost programs are typically justified by ROI thresholds. If a model deployment reduces back-office labor by $10 million annually, the infrastructure supporting that deployment is unlikely to be cut in a downturn. It becomes embedded in operating efficiency.

Peripheral SaaS tied to incremental hiring or discretionary departmental budgets does not have the same internal protection. During liquidity tightening, those budgets are reviewed first.

From a capital allocation standpoint — especially for allocators managing multi-currency reserves or sovereign capital where preservation and duration matter — this difference in internal budget classification becomes critical.

One layer of revenue is classified as operating necessity.

Another is classified as discretionary enablement.

Over long horizons, that difference widens dispersion.

Now consider currency stability and liquidity regimes.

In tighter global liquidity environments, enterprises prioritize free cash flow generation and margin stability. Sponsor-controlled portfolios intensify oversight. Cost programs accelerate. AI embedded in restructuring mandates becomes a tool for protecting margins against currency volatility and financing cost variability.

Infrastructure revenue tied to measurable efficiency thus carries lower sensitivity to discretionary budget contraction. Seat-based SaaS tied to workforce expansion carries higher sensitivity.

For allocators operating across AED, CHF, USD or other reserve exposures, the key question is not “Which AI company grows fastest next quarter?” It is “Which revenue streams remain justified when financing conditions tighten and boards demand cash flow stability?”

The staffing data suggests that enterprise AI is increasingly embedded in the latter category.

After looking at the workforce composition of these companies, we can also widen the lens further.

Private equity operating teams expanded materially during a period of constrained exits. That says to me this is the signal of value creation. Restructuring and capital advisory firms expanded materially, signaling throughput of cost and capital realignment programs. Workflow and procurement vendors expanded in alignment with process standardization and cost visibility. AI-native platforms scaled engineering and integration capacity. Offshore labor did not explode. Broad seat-based SaaS did not enter any kind of true euphoric expansion.

That alignment indicates a structural pivot.

The productivity lever is changing from labor multiplication to labor compression enabled by automation. And no, I am not talking the AI excuses given for layoffs… I’m just calling it for what it is… a capital allocation claim.

When sponsors standardize AI stacks across portfolios, vendor concentration increases, control plane systems gain stickiness, peripheral tools face review and revenue dispersion widens.

Now think about that five-year duration again.

If sponsor enforced automation reduces labor cost by 3–5% across large enterprises, and if vendor stacks consolidate by even 5–10% at the edges, growth normalization for seat-based SaaS becomes structural rather than cyclical. Infrastructure and workflow embedded in enforcement programs retain budget protection. That divergence compounds over time.

Return to my thesis.

Whoever controls the consultant controls enterprise AI spend.

Consultants write restructuring decks.

Sponsors increasingly control consultants through expanded internal operating teams.

The workforce data shows sponsor capacity thickening materially.

And all of that means consultants operate inside tighter capital mandates.

When AI partnerships are embedded in that consultant layer, AI spend becomes embedded in capital structure decisions rather than discretionary experimentation.

The question is no longer “Is AI growing?”

The question becomes:

Where is AI embedded inside non-discretionary capital enforcement?

Which revenue streams sit closest to mandated cost reduction?

Which revenue streams depend on hiring growth and departmental discretion?

Which layers gain concentration as portfolios standardize?

Which layers lose share as stacks compress?

Authority has moved upstream.

Capital follows authority.

When authority consolidates, spend consolidates.

When spend consolidates, dispersion increases.

The staffing footprint I’m seeing across the institutional stack is coherent.

Not headlines. Not WARN notices. Not quarterly beats. Not even product demos.

Authority.

It’s about authority.

And today…. Whoever controls the consultant controls enterprise AI spend.