Energy Vault’s Moment Is Now

The 30% Upside the Market’s Sleeping On

Energy Vault Holdings (NYSE: NRGV) is trading at a steep discount despite clear signals of operational turnaround. With a 31.5% workforce reduction, no debt, and a 14-year $20M/year energy storage contract (LTESA) entering revenue ramp, the company is structurally leaner and better positioned than its peers. Analysts haven’t caught up, and short interest (21.6%) makes this a prime candidate for a post-earnings revaluation. This piece lays out why the next leg could take NRGV to $1.50+ - and what to watch for.

Energy Vault’s (NRGV) 2024 10-K drops March 17, alongside Q1 earnings, and at $1.15, I am at a loss of why nobody is excited for this one. Granted…. you have to be made of strong stuff in the current market, but the upside is worth it.

Here’s what’s not priced in:

31.5% workforce reduction (down to 183 employees) → Leaner, more efficient operations.

14-year Long-Term Energy Service Agreement (LTESA) for Stoney Creek (1 GWh, $20M/year) → Locking in revenue stability.

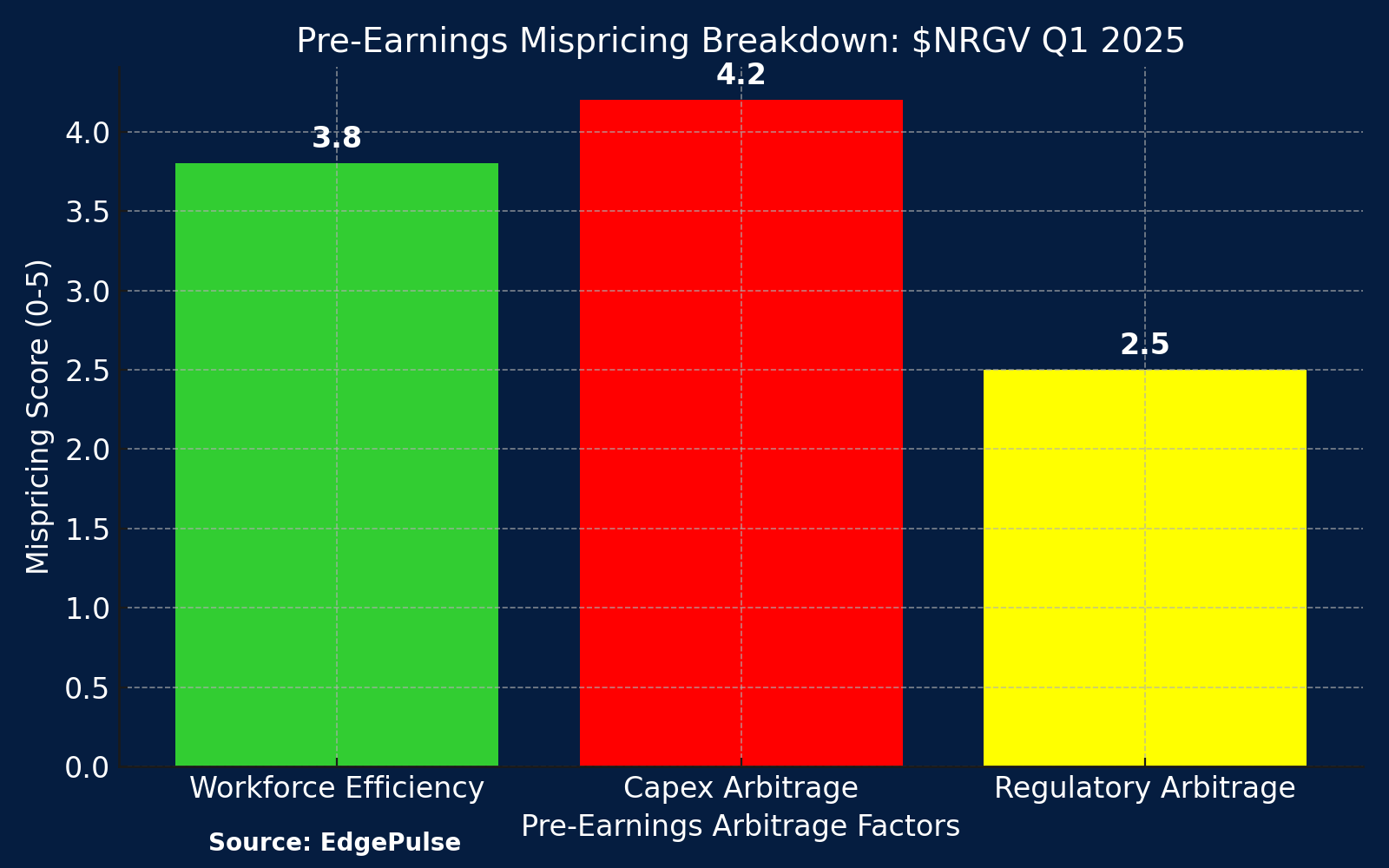

Short interest is 21.6%, and analysts aren’t catching the efficiency arbitrage. My modeling suggests a 75% chance of outperformance, with a potential initial upside of $1.25-$1.40 and potential to reach $1.50+ by Q3.

Energy Vault is optimizing for growth. The market catches up fast. Will you be ahead of it?